When Real Rates Rise and Breakevens Fall, Corporate FX Risk Changes

When Real Rates Rise and Breakevens Fall, Corporate FX Risk Changes

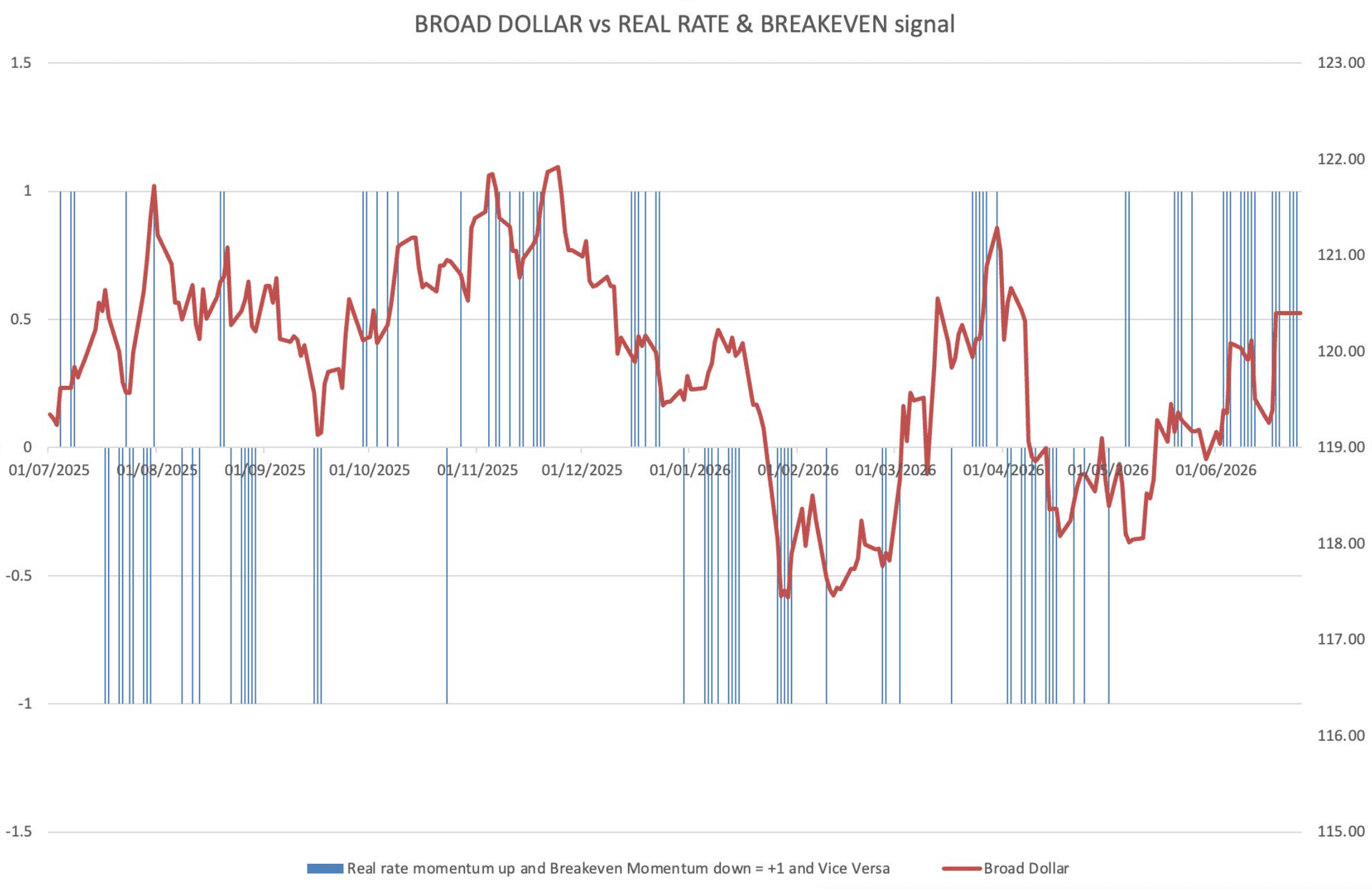

This chart captures an important USD setup.

When US real rate momentum is rising while inflation breakeven momentum is falling, the dollar usually has a tailwind.

For corporates, that matters.

A stronger dollar can quickly affect import costs, overseas revenues, balance-sheet translation, covenant ratios, hedge effectiveness, and budget rates.

In the current type of regime, the dollar can rise for a more constructive reason: US growth is outperforming, and US real yields are rising because the US economy is proving more resilient than others.

That is the “US exceptionalism” version of dollar strength.

Higher real yields mean global investors are paid more, after inflation, to hold US assets. Lower breakevens mean the market is not simply pricing an inflation scare. The signal is cleaner: stronger real returns, contained inflation expectations, and a Fed with less reason to rush into easing.

For companies with USD exposure, this matters because the dollar can strengthen even without a crisis.

The two regimes can also overlap. If higher US real rates eventually tighten global financial conditions enough to hurt risk appetite, the dollar can receive a second tailwind: the safe-haven bid.

So the sequence can be:

USD rises because US real returns improve.

USD rises further if global risk appetite deteriorates.

FX risk can move quickly from “manageable” to “material”.

High-beta EM FX

USD/ZAR, USD/BRL, USD/COP, USD/CLP, USD/HUF and USD/PLN can move sharply higher as US real yields rise and investors cut EM exposure.

Carry favourites

USD/MXN is important. Mexico may have strong fundamentals, but crowded carry trades can unwind when US real yields rise.

Commodity and China-sensitive FX

AUD/USD and NZD/USD usually struggle. They are liquid expressions of global growth, China demand, and risk appetite.

Low-growth G10 FX

EUR/USD tends to weaken when US growth and real-rate differentials move in favour of the dollar. GBP/USD and USD/SEK often follow the same logic.

JPY and CHF are more nuanced. Yield spreads favour USD, but safe-haven flows can offset some of that.

For corporates, the practical question is not just “where is spot today?”

It is:

*Are budget rates still realistic?

*Are hedge ratios still appropriate?

*Which exposures are most vulnerable if USD strength broadens?

*Do we understand second-order impacts on suppliers, customers, and margins?

*Are we prepared for a regime where USD rises without an obvious risk-off trigger?

The simple framework:

FX = growth differential + real yield differential - risk sensitivity

When all three point toward the US, the dollar does not need panic to rally.

Sometimes it only needs stronger US growth, rising real yields, and contained inflation expectations.

#FX #CorporateTreasury #Treasury #CFO #RiskManagement #CurrencyRisk #USD #Dollar #Macro #RealYields #Breakevens #Hedging #EmergingMarkets #G10FX #USExceptionalism #GlobalMarkets