US exceptionalism.......is the USD going to lift again???

The US is simultaneously experiencing:

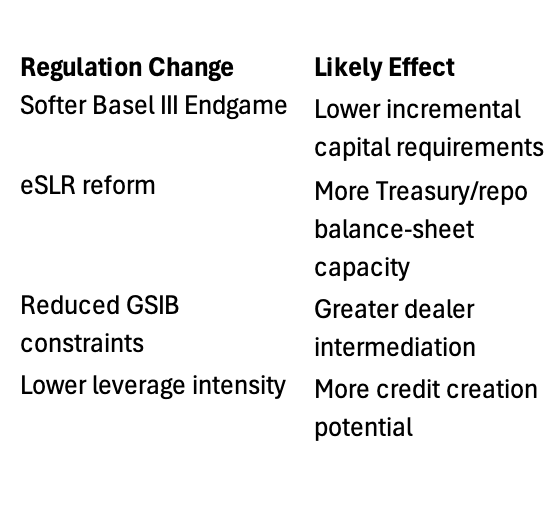

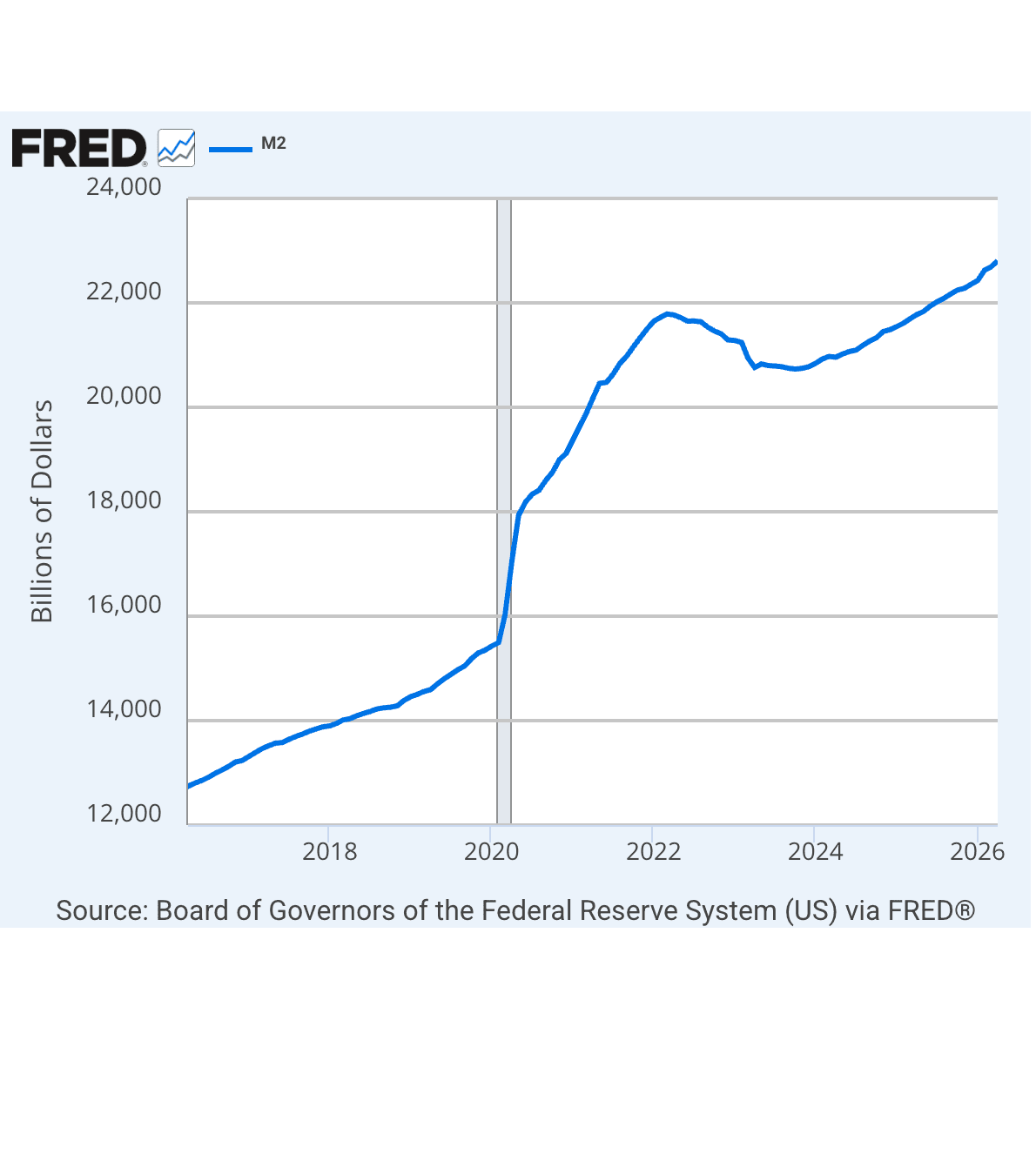

Major bank balance-sheet deregulation, a hyperscaler AI capex boom, enormous fiscal stimulus, and improving financial liquidity architecture.

The market keeps looking at policy rates and asking why growth has not rolled over. But perhaps rates are no longer the dominant variable.

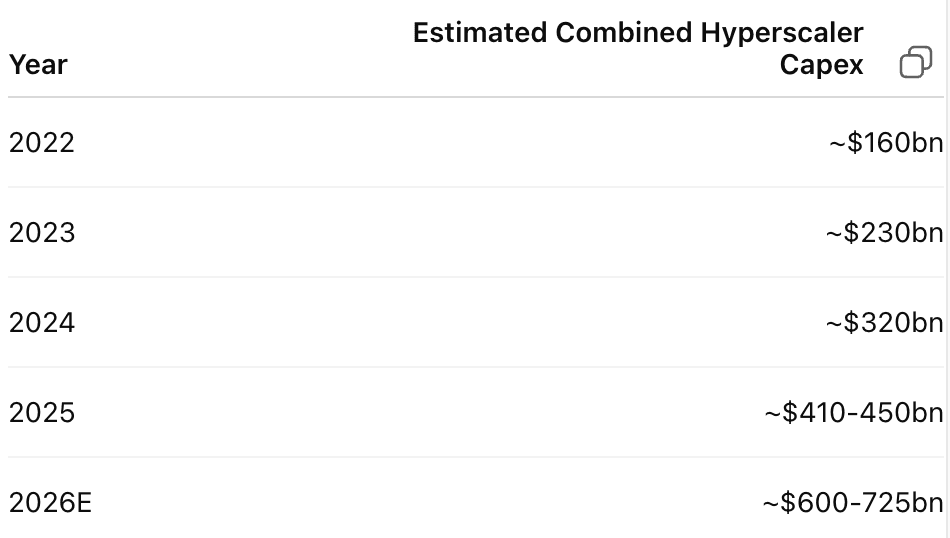

If banks are gaining balance-sheet capacity just as the likes of Microsoft, Amazon, Alphabet and Meta Platforms embark on a multi-trillion-dollar AI infrastructure buildout, then the US may be entering a new phase of liquidity-supported investment expansion.

We all know this is not just a tech cycle.

It touches:

power grids, semiconductors, construction, credit creation, industrial capacity, data centres, engineering, and capital markets.

Now compare that backdrop with the rest of the world.

China,

still possesses extraordinary manufacturing scale, world-class infrastructure, dominance in EVs, batteries and parts of green technology, and the ability to mobilise capital quickly when policymakers choose to act. But the economy is also navigating the aftermath of a major property and credit cycle, weaker demographics, and softer private-sector confidence.

Europe,

retains major strengths in high-end manufacturing, luxury goods, pharmaceuticals, aerospace, industrial engineering and the energy transition. Germany’s industrial base, French luxury and aerospace leadership, and Nordic innovation ecosystems remain globally competitive. But Europe also faces tighter fiscal constraints, fragmented capital markets, higher energy costs and less hyperscaler dominance in AI infrastructure.

The contrast is becoming difficult to ignore and the valuation gap has eased over the past 12 months. The US is increasingly acting like the only major economy capable of simultaneously generating:

- deep capital markets,

- sovereign-scale private investment,

- fiscal expansion,

- technological leadership,

- energy abundance,

- and global reserve currency demand.Regulation Change

That starts to look a lot like US exceptionalism again.

The big question I need to answer is will we move back toward the middle of the Dollar Smile. The fact that the USD has not been weakening significantly when oil prices fell suggests the answer could be we will.