Slow motion car crash.....Japanese debt.... FX hedges

Slow motion car crash.....Japanese debt.... FX hedges

I am sure a lot of you remember what it was like 2007 to 2008 anyone in a investment seat could see at least some of the GFC issues in markets but none of us knew how it would unravel.

I am telling my clients to be fully buttoned up on fx hedges because the Japanese set up will be a large issue for all markets but FX escpecially.

Why the crisis is already here.

Current coupon payments mean......

Interest / tax receipts: ~16%

Interest / GDP: ~2.1%

Interest payments: ~¥13.1 trillion

Tax receipts: ~¥83.7 trillion

Using the current JGB curve;

of the outstanding debt, the implied interest cost is closer to:

~¥25.5 trillion

That would be:

~30% of tax receipts !!!!!!!!!!

~4% of GDP

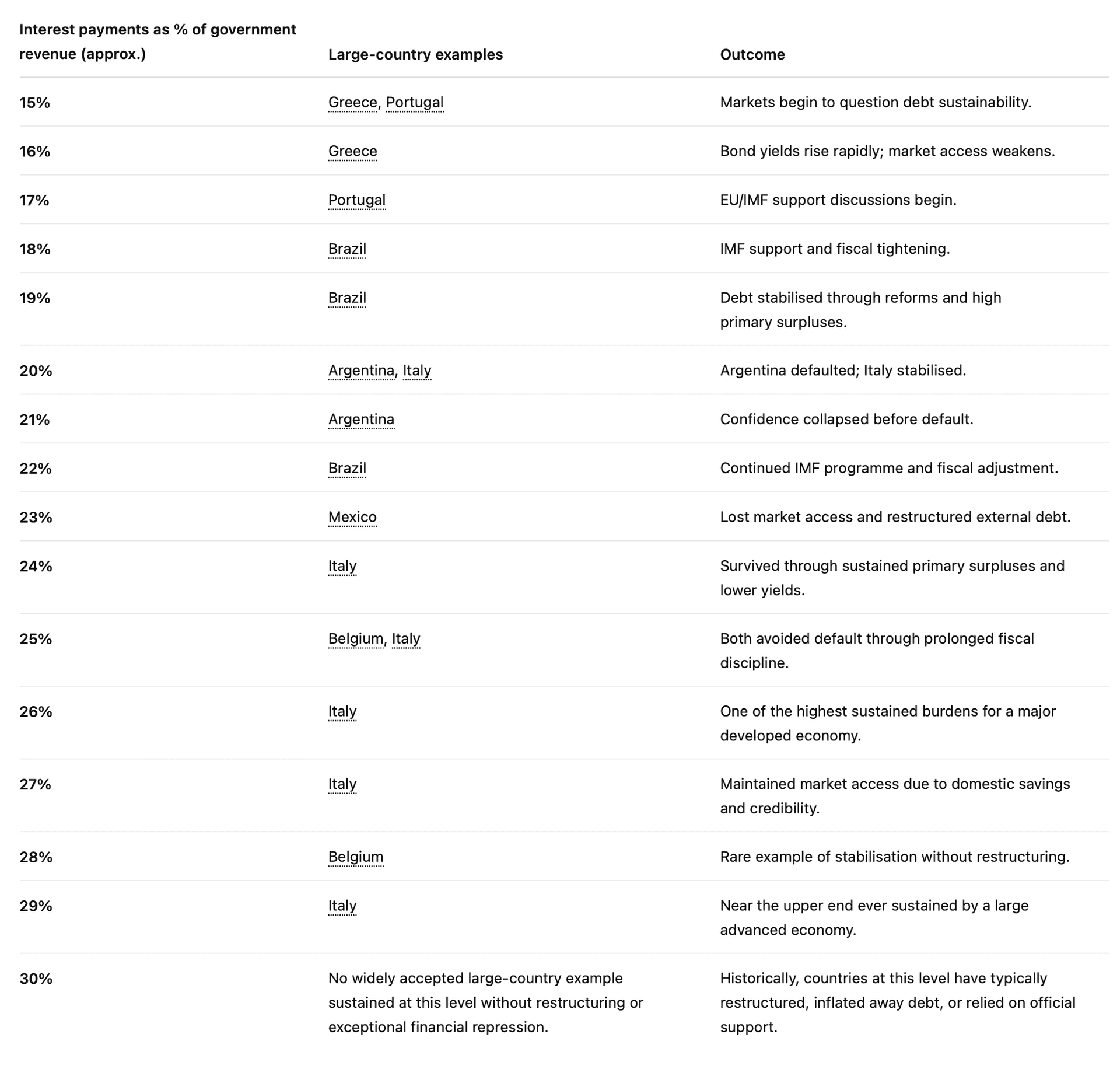

What the history tells us.

This table illustrates a pattern rather than a precise threshold:

15–20%: Many sovereign crises begin if growth slows or borrowing costs rise.

20–25%: Outcomes diverge. Countries with strong institutions (Italy, Belgium) can survive; weaker sovereigns often lose market access.

25–30%: Extremely few large economies have sustained these levels. The principal exceptions are Italy and Belgium in the late 1980s and early 1990s.

30%+: There are essentially no major developed economies that have maintained this burden for long without debt restructuring, very high inflation, financial repression, or substantial external assistance.