New JPY intervention.... worth betting against?

Japan may not look like the UK on the surface. However from an FX perspective, the comparison is becoming harder to ignore.

For years, the dominant macro narrative around Japan has rested on one reassuring fact:

“Japan owns its own debt.”

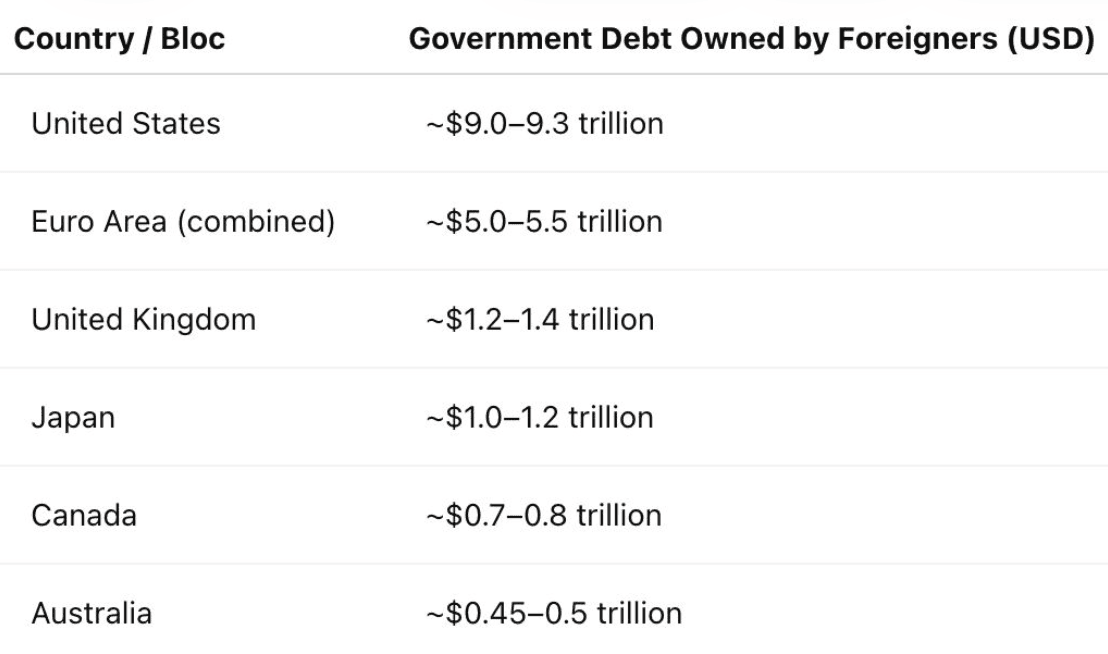

Only around 10–12% of Japanese government debt is foreign-owned versus much higher external ownership across other developed bond markets.

That statistic has been treated as structural immunity.

But markets trade flows, not percentages.

Because Japan’s debt pile is so enormous, foreign investors still own roughly $1–1.2 trillion of JGBs — broadly comparable in absolute size to foreign ownership of the UK gilt market.

solid counterpoint is a meaningful share of foreign JGB ownership is probably “sticky” capital:

• reserve managers

• central banks

• passive bond index allocators

• benchmark-constrained real money investors

Those investors are not typically prone to sudden liquidation.

But I still think the market underestimates the significance of the absolute size of the foreign position embedded inside Japan.

Especially because the character of the JGB market appears to be changing.

For decades Japan benefited from:

• persistent current-account surpluses

• enormous domestic savings

• captive institutional buyers

• and a BOJ willing to suppress volatility aggressively

That architecture allowed Japan to sustain debt near 230% of GDP without suffering the type of funding stress associated with externally dependent economies.

JGB market behaviour has become increasingly asymmetric.

When global disinflationary conditions emerge, Japanese yields barely rally.

But when global yields rise or inflation pressures reappear, JGB yields react much more aggressively.

That asymmetry matters.

The yen has already undergone a prolonged stealth devaluation on a real effective basis despite:

• a persistent current-account surplus

• and one of the world’s largest positive NIIPs

That is unusual.

It strongly suggests the market has already embedded a meaningful fiscal and monetary risk premium into JPY over time.

Is JPY already mostly priced?

Or is the market still underestimating what happens if:

• BOJ control weakens further

• duration volatility rises structurally

• and the marginal buyer of JGBs becomes more price-sensitive?

My own view is that the eventual adjustment mechanism probably involves:

• higher domestic yields

• a weaker yen initially

• and only later meaningful repatriation flows

The stress likely comes first.

The stabilisation mechanism comes later.

The vulnerability may not resemble a classic UK-style balance-of-payments crisis. Japan’s funding structure however does not make it immune to external pressure.

#Japan #JPY #Yen #BOJ #JGB #FixedIncome #Macro #FX #Rates #BondMarket #GlobalMacro #CurrencyMarkets #Investing #Economics #InterestRates #CentralBanks #Volatility #CapitalFlows #AssetAllocation #Markets