JPY Intervention risk very high!

USD/JPY volatility: why finance teams should be watching Satsuki Katayama

For CFOs and Finance Directors with yen exposure, the key question is not whether Japanese officials are uncomfortable with USD/JPY.

They clearly are.

The more useful question is: which official comments actually matter for hedge timing and volatility risk?

At Dragten Capital Solutions, we think Finance Minister Satsuki Katayama is the official to watch most closely.

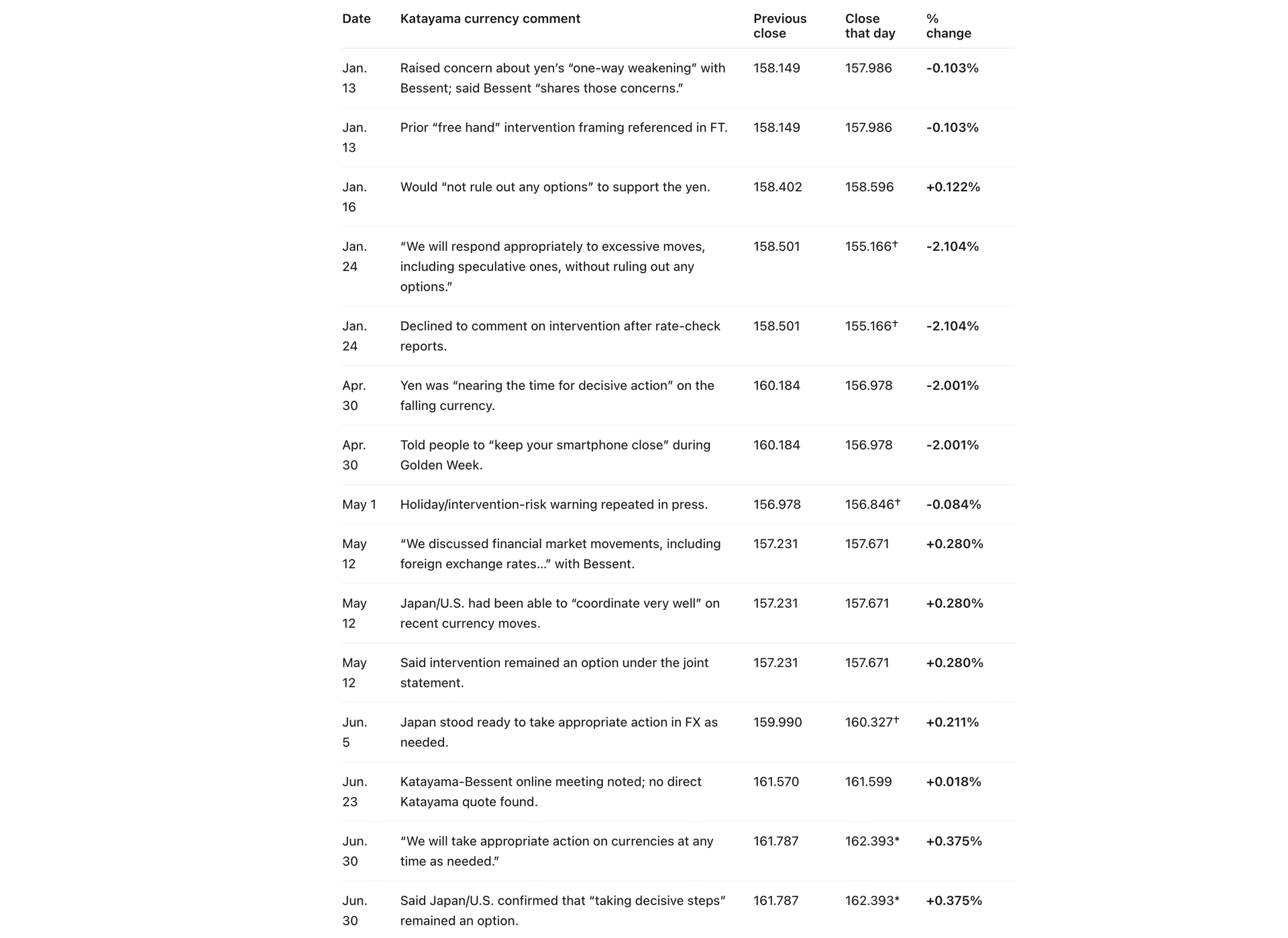

Her comments have timed most closely with actual intervention risk. In April, as USD/JPY moved through the 160 area, Katayama warned that Japan was nearing the point for “decisive action” on the falling yen. She also warned market participants to keep their phones close during Golden Week.

That was not just background noise. USD/JPY subsequently fell sharply, with the yen strengthening by roughly 2% on a close-to-close basis.

This matters for corporates because intervention risk does not move in a straight line. It tends to appear suddenly, around key levels, after repeated official warnings, and often when liquidity is poor. That can create large overnight moves in hedge valuations, budget rates, and unhedged payables or receivables.

Katayama has been relatively quiet since the April episode, but in the last 24 hours she has reaffirmed that Japan will take appropriate action on currencies as needed. She also referenced U.S.-Japan coordination and the possibility of “decisive steps.”

That should get the attention of any finance team with JPY exposure.

USD/JPY had already made new closing highs earlier in June, around the 8th, without immediate intervention. But the latest move is different. The yen is weakening again while U.S. rates further out the curve are not providing the same clear justification. That increases the sense that Japanese officials may see the FX move as excessive rather than simply rate-driven.

For CFOs and Finance Directors, the takeaway is practical:

This is not about predicting the exact timing of intervention.

It is about avoiding being forced to hedge after volatility has already arrived.

When official language moves from “monitoring” to “excessive moves,” then to “no options ruled out,” and finally to “decisive action,” hedge ratios should be reviewed before the market gaps, not after.

For companies with yen costs, yen revenues, yen debt, or Japanese supplier exposure, now is a good time to reassess:

Are hedge ratios still aligned with budget rates?

Would a 2-3% overnight move in USD/JPY create a P&L or cash-flow issue?

Are hedge maturities too concentrated around potential intervention windows?

Is there enough flexibility to adjust if the Ministry of Finance steps in again?

At Dragten Capital Solutions, we help finance teams translate policy signals into practical hedge decisions. The goal is not to speculate on intervention. The goal is to reduce avoidable FX volatility before it reaches the income statement.

#DragtenCapitalSolutions #CFO #FinanceDirector #Treasury #FXRisk #USDJPY #JPY #Hedging #CurrencyRisk #CorporateTreasury #RiskManagement