How many G10 central bankers does it take to change a lightbulb?

How many G10 central bankers does it take to change a lightbulb?

Just one. But they will hold rates steady for two years to see if the lightbulb changes itself.

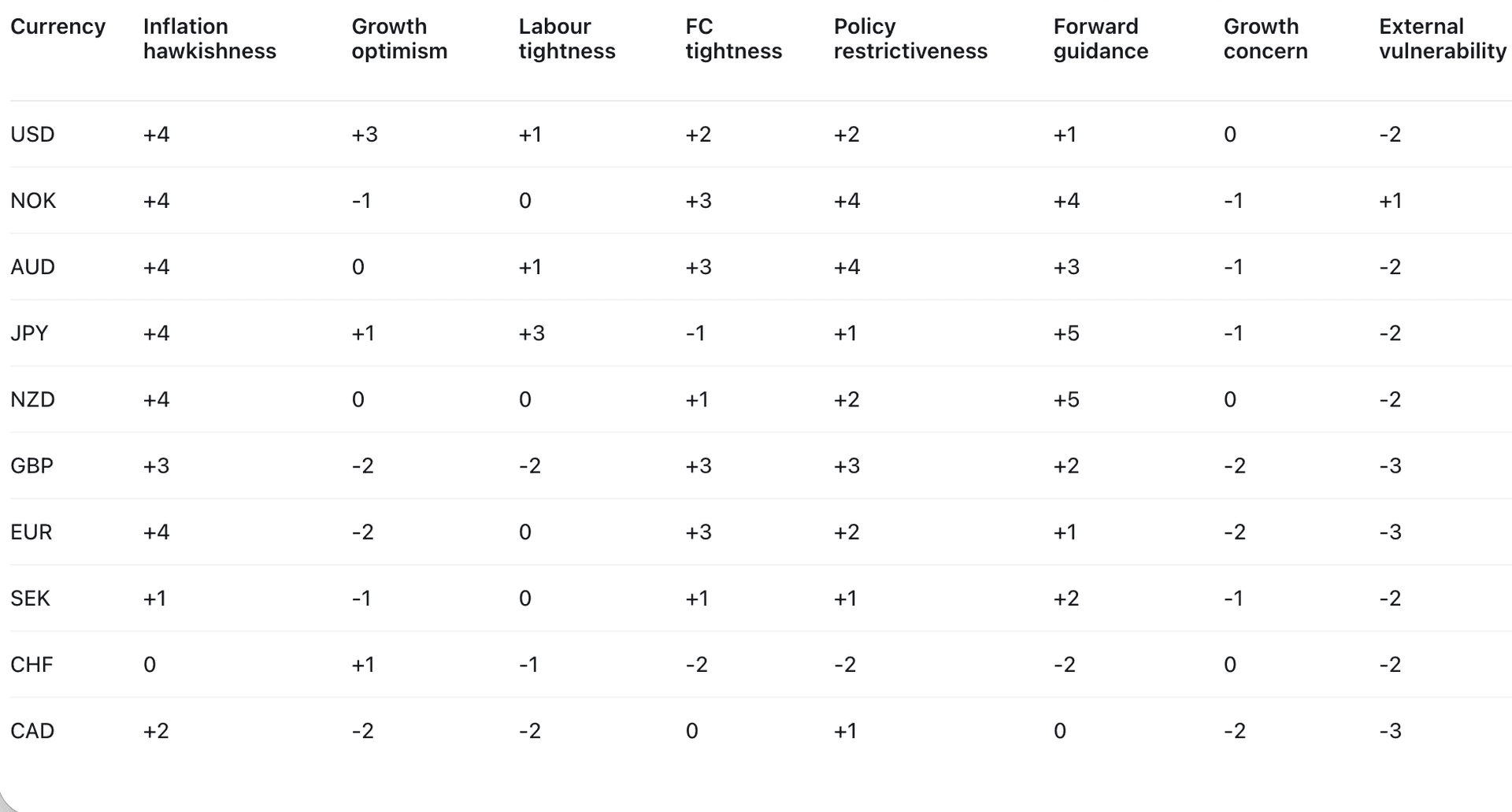

Central bank language is starting to matter again for FX, but not all “hawkish” signals are equal.

I scored the latest G10 central bank communications using a language only framework across inflation concern, growth optimism, labour tightness, financial conditions, policy restrictiveness, forward guidance, growth concern and external vulnerability.

I also double-weighted growth, because in this environment the question is not just “who sounds hawkish?” It is “whose economy can absorb tighter policy?”

On this basis, the strongest language support sits with:

USD

NOK

AUD

JPY & NZD

The key point is that USD screens best not because the Fed has delivered a fresh hawkish shift. It has not. The Fed minutes look more like hawkish continuity. But the Fed combines elevated inflation concern with the strongest growth language in the G10 set: solid activity, resilient consumption and strong AI-related investment.

JPY is a special case. The 200+ % of gdp debt and currently rising rates puts it at idiosyncratic risk.

The other important point: Europe is unloved in this framework.

EUR, GBP, SEK and CHF all screen poorly or only neutrally.

Why?

EUR has inflation concern, but weak growth language. The ECB is worried about upside inflation risks, but also about downside growth risks, weaker confidence, tighter credit and energy-price damage. That is not a clean currency-supportive mix.

GBP has a hawkish tail, with two BoE members voting for a hike. But the UK growth and labour language is soft: subdued underlying momentum, loosening labour market, weak demand and tighter household financing conditions. The market can respect the inflation risk while still disliking the growth backdrop.

SEK has only modest support. The Riksbank acknowledges higher inflation risk and a greater probability of a rate rise later this year, but inflation is still below target and activity is weaker than normal. That makes the signal cautious rather than forceful.

CHF is the weakest European signal. The SNB is at 0%, inflation is still within the price-stability range, and the central bank explicitly signals willingness to lean against excessive franc appreciation. From central-bank language alone, that is a clear headwind.